Do you know the importance of keeping good business financial records? The first one that might come to mind is to make the annual income tax reporting process go as smooth as possible. That is certainly a very good reason to keep the company bookkeeping records accurately up-to-date but there are many equally important reasons to stay ahead on this important business function.

All businesses should routinely check their company’s General Ledger for important information. The easiest way to check all of the accounts in the company general ledger is to frequently create and check the Balance Sheet, Income Statment, and Statement of Cash Flows. These reports are easily generated with accounting software such as QuickBooks but are only as accurate as the transactional data entered into the company file.

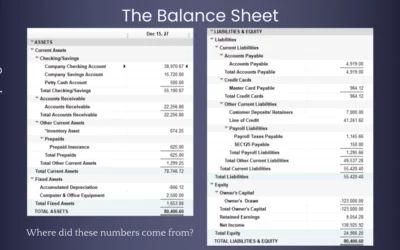

We will first take a look at the company’s Balance Sheet, a snapshot of what the company

You also need to pay attention to your liability accounts for possible trouble signs, for instance, tax liabilities, especially payroll taxes, to avoid late fees and penalties. The Balance Sheet also tells us our Working Capital ratio: Current Assets divided by Current Liabilities. We get these totals from the Balance Sheet and WC ration of 1 means we are in trouble.

The company Income or Profit and Loss Statement tells us how well your sales efforts are doing compared to the cost of those sales efforts. It is easy to create an expense report to keep an eye on costs involved with the operation of your business. Every manager should keep an eye on expense for possible areas of savings as well as

The Statment of Cash Flows takes a look at cash coming and going for a defined period. It takes information from the Balance Sheet and the P&L to give us three categories of cash in and out of our business. This report requires us to use an Accrual basis of accounting versus a Cash basis.

For more information on setting up your company’s bookkeeping and accounting system, call Charley and Manny at C&M Bookkeeping today.

0 Comments